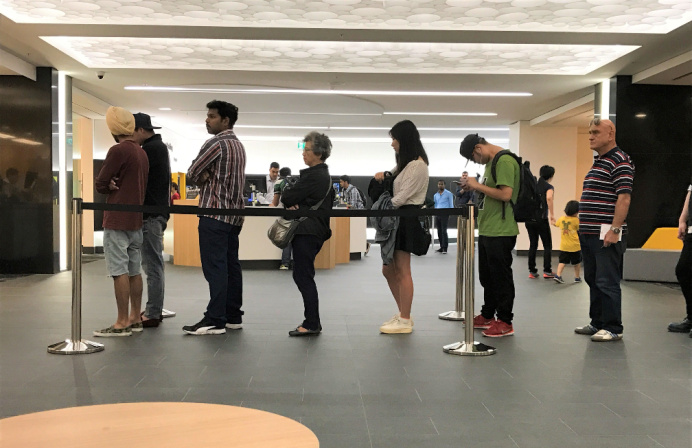

Most Australian banking customers are still seeking out physical bank branches, with 72 per cent of respondents to a recent survey reporting that they have visited a branch in the past six months.

At least one in three Australians reported visiting a physical branch in the last month, according to the Publicis Sapient Customer Banking Report 2024, which surveyed more than 5,000 Australians on their banking habits and current views of the industry.

Only 17 per cent of respondents reported that they had not visited a bank branch in over a year.

“Banks envision a future where most financial interactions occur through digital channels, with physical channels reserved for key sales and service interactions – but this is at odds with the expectations of large parts of the population,” the report read.

Cash services are among two of the top three services that customers expect at a branch, indicating that, despite the digital payments push and strong uptake of digital wallets among Australians, there is still demand for cash transactions.

While Covid-19 restrictions no doubt “turbocharged” digital or cashless payments in Australia, a majority of customers (70 per cent) stated that they were not in favour of eliminating cash services from branches, with more than three in four customers (76 per cent) stating that they still carried cash on them.

While most (76 per cent) expressed disfavour with paying extra to have cash transactions available at their local branch, nearly a quarter of respondents (24 per cent) stated they were willing to pay roughly between 0.1 per cent and 5 per cent for continued access to cash services.

Among the top three available services customers expected at their local bank branch were: ATMs (66 per cent), customer service (60 per cent) and deposits/withdrawals (60 per cent). Lending (51 per cent) and account services (50 per cent) rounded up the top five.

The latest data from the APRA shows a progressive drop last year in the number of bank branches, with 424 branches closed Australia-wide; among these, 122 branches were shuttered in regional and remote areas.

From mid-2017 to 2023, the number of physical branches has declined by more than one-third, with regional and remote areas experiencing the same rate of decrease over this period.

One of the key concerns among customers of a fully digitised experience and payments services was the fear of service outages.

“Outages were a common concern among customers in our research – both due to IT service issues and power or telecom network downtime,” the report read. “Allaying these concerns will be important for banks to shift customers to card and digital payment methods.”

Further, a major outage could create a serious setback for customer faith in cashless payments, with around a third (34 per cent) of respondents stating they would consider switching banks based on a digital outage.

Half of the respondents (50 per cent) said they had experienced a service outage using a card or digital wallet at least once, while nearly one in three (31 per cent) reported experiencing multiple outages.

Banks, it was argued, must seek to effectively balance the demand for personalised services – traditionally received through in-branch experiences – in an increasingly digitised world.

Indeed, the report found that nearly three out of four respondents (74 per cent) expect banks to offer personalised services and conversations; however, customers tend to associate these expectations with physical channels (i.e. branches) rather than digital ones.

The advent of artificial intelligence (AI) technologies, the report read, has “opened for banks to innovate and simplify with new business models, deploy tools for enterprise enablement and, in particular, provide elevated personalised customer experiences”.

However, only a slight majority of Australians (58 per cent) believe that AI will improve the level of service from their bank, while almost all Australians (96 per cent) expressed concerns about banks using AI technology.

Notably, older customers who would benefit from personalised support to help them transition to digital offerings, are also the ones most cautious of AI.

Chief among customers’ concerns in response to banks’ ready adoption of AI was a preference to speak with a human being (58 per cent), the potential loss of jobs (54 per cent), and data security and privacy (49 per cent).

“This demonstrates the potentially limited awareness of AI capabilities and a lack of understanding of the difference between chatbots, automated phone calls and broader applications of AI,” Publicis Sapient wrote.

“Sentiment towards AI is caught between giving the technology a chance to offer better, more personalised service, and the frustration of it not resolving queries at the same level a human would.”

For Tales Sian Lopes, head of financial services, Australia & New Zealand at Publicis Sapient, one of the key challenges for Australian banks attempting to utilise AI is to ensure that it can “deliver the personalised services that people are increasingly demanding whilst also showing customers that they are engaged in the safe and ethical application of these fast-emerging technologies”.

“There is an enormous opportunity for banks to proactively design a better customer experience,” he added.